Upstream spending will struggle to recover to pre-pandemic levels

The toll of the Covid-19 pandemic on upstream investments in the first two years of the downturn is estimated at a whopping $285bn, and although spending will slowly start to rise from 2022, it will not reach pre-crisis levels in the coming period, according to a Rystad Energy report. The shale sector has been the most affected, with conventional exploration and investments in mature assets suffering the least thus far.

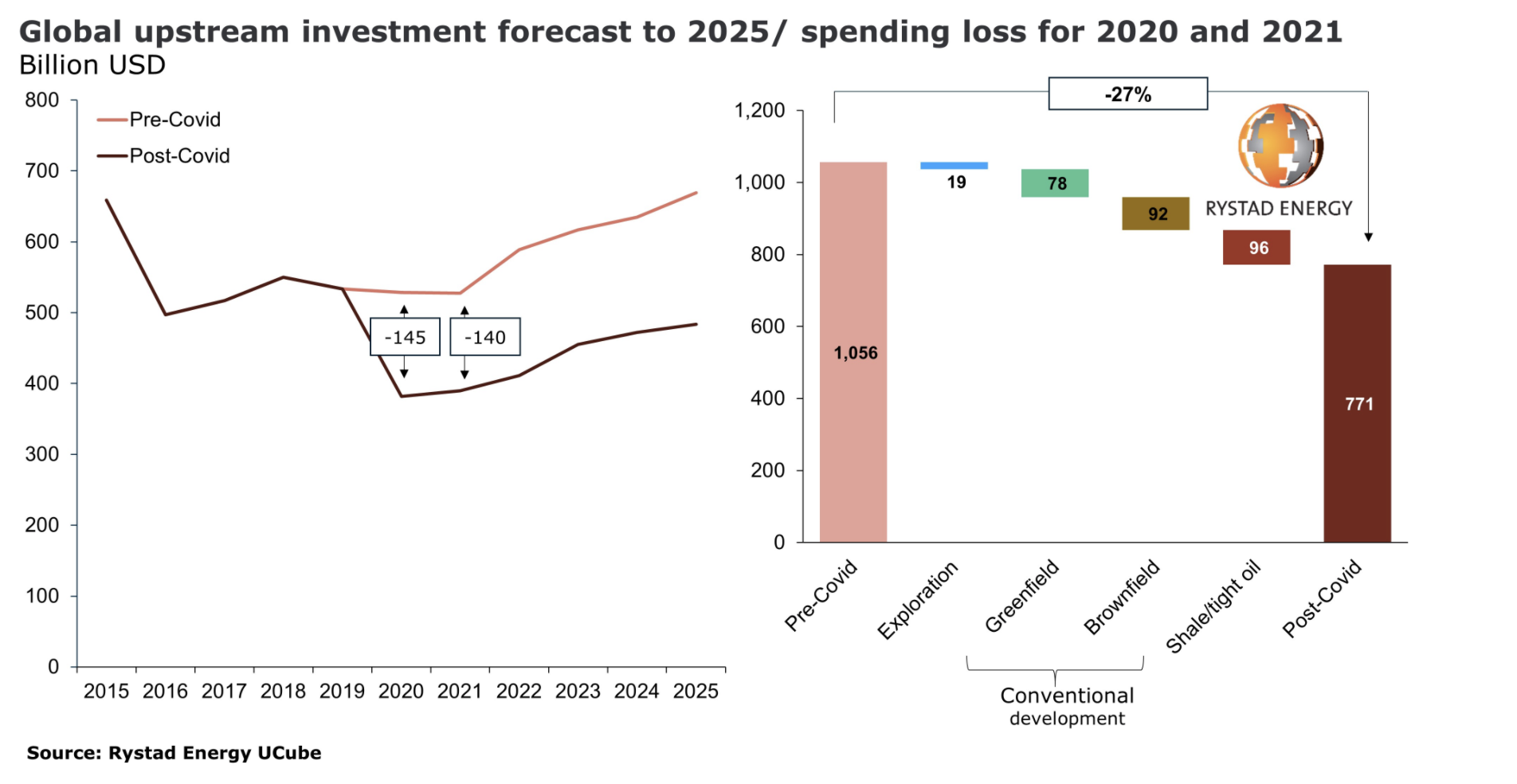

In February 2020, before Covid-19 started impacting the global energy system, Rystad Energy estimated global upstream investments for the year would end up at around $530bn, almost at the same level as in 2019. Our forecast at the time suggested 2021 investments would remain in line with the previous year’s level.

|

Advertisement: The National Gas Company of Trinidad and Tobago Limited (NGC) NGC’s HSSE strategy is reflective and supportive of the organisational vision to become a leader in the global energy business. |

However, as the Covid-19 pandemic triggered a collapse in oil prices during the early part of the second quarter last year, E&P companies slashed investment budgets to protect cash flow. This spending trend was not reversed in 2021, when prices rose. Compared to pre-pandemic estimates for 2020 and 2021, we observe that spending fell by around $145bn last year and will end up losing $140bn by the end of this year. This implies Covid-19 removed 27% of planned investments.

Upstream spending was limited to $382bn in 2020 and is forecast to marginally grow to $390bn this year. Rystad Energy expects the effect of the pandemic to be a lasting one as – even though spending will start growing from 2022 – it will not return to the pre-pandemic level of $530bn. Growth will be limited and investments will only inch up annually, rising to just over $480bn in 2025, when this report’s forecast ends.

Learn more in Rystad Energy’s UCube.

Over the two-year period between 2020 and 2021, shale/tight oil investments are the ones most affected in both absolute and percentage terms, losing $96bn of the previously expected spending, or 39% for the sector. Exploration spending is expected to drop by $19bn, or 22%, compared to what was previously forecast. Greenfield investment in new conventional projects will suffer a $78bn loss, or 28%, while brownfield investment in existing such projects will fall by $92bn, or 20%.

“Since shale/tight oil is both the segment with the highest decline in activity and the supply source in greatest need of continuous reinvestment to keep production growing, the immediate impact on output from this sector has been significant,” says Espen Erlingsen, head of upstream research at Rystad Energy.

For more analysis, insights and reports, clients and non-clients can apply for access to Rystad Energy’s Free Solutions and get a taste of our data and analytics universe.

The statements, opinions and data contained in the content published in Global Gas Perspectives are solely those of the individual authors and contributors and not of the publisher and the editor(s) of Natural Gas World.