Supply concerns hit the European gas market

European gas prices jump higher

The European gas market had been looking as though it was in better shape. Storage was filling up at a good pace, which saw the gap in inventory levels narrowing significantly to the 5-year average. This in turn saw prices coming off from the high levels we saw following Russia’s invasion of Ukraine. However, this has changed abruptly this week. TTF prices have rallied by around 50%, which has taken prices back above EUR120/MWh - levels last seen back in early March. The catalyst for the move has been reduced Russian gas flows via the Nord Stream pipeline, along with the potential for reduced LNG arrivals after an outage at the Freeport LNG terminal in the US. Warmer weather across parts of Europe will also be providing some support.

|

Advertisement: The National Gas Company of Trinidad and Tobago Limited (NGC) NGC’s HSSE strategy is reflective and supportive of the organisational vision to become a leader in the global energy business. |

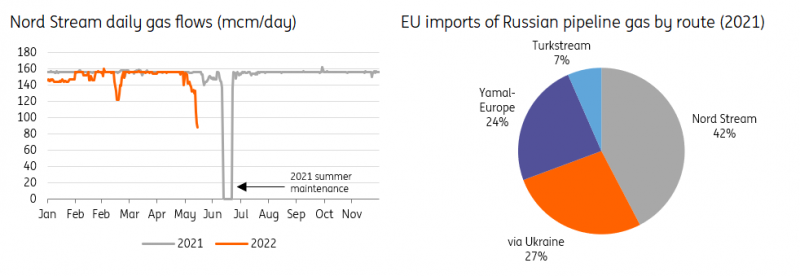

Nord Stream flows plummet

Gas flows via the Nord Stream pipeline have started falling significantly in recent days. This is after Gazprom warned that flows would be reduced as much as 40% due to delays in receiving a turbine which had been undergoing maintenance in Canada. Sanctions against Russia has made it difficult for this to be returned. However, since then Gazprom has reported an outage for another compression turbine, which would see gas flows falling even further along the pipeline - to as low as 67mcm/day compared to the roughly 155mcm/day we usually see. The latest data shows that flows fell to a little under 88mcm/day on 14 June. Clearly with the latest announcement these will fall further.

This reduction is significant for Europe. The Nord Stream pipeline is the largest source of Russian gas for Europe, with annual volumes of around 58bcm, and around 40% of total Russian pipeline flows to the EU.

Adding to supply concerns is that the Nord Stream pipeline was already set to undergo its usual summer maintenance between 11-21 July, which will see flows coming to a complete standstill. The disruptions we are seeing now suggest the potential for a prolonged period of significantly reduced flows via the pipeline.

Gazprom could increase flows via Ukraine to try make up for the Nord Stream shortfall. However, up until now there is no indication that they are willing to do this. In addition, flows via the Yamal-Europe pipeline have been flowing eastwards for several months rather than the usual westerly direction.

Nord Stream is crucial for Russian gas flows to Europe

Source: ENTSOG, EC, ING Research

Freeport LNG outage

The disruptions to Nord Stream gas flows follow supply concerns in the LNG market. This is after a fire at the 15mtpa (roughly 20bcm) Freeport LNG export terminal in the US. The fire will see the plant offline for a period of 90 days, significantly longer than the 3 weeks that was initially expected. Freeport LNG made up around 18% of total US LNG exports in March. Europe has increased its reliance on US LNG recently (around 70% of US LNG exports were shipped to the EU+UK in March) due to reduced Russian flows. In March, Freeport exported around 1.8bcm, of which around 1.3bcm went to the EU+UK. Whilst not significant relative to Nord Stream flows, it certainly doesn’t help at a time when Europe is needing to rely more on the LNG market for supply.

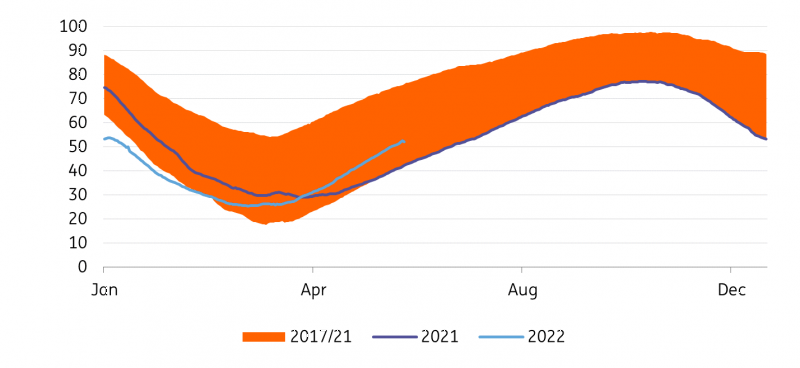

How will this impact storage levels?

Storage levels in Europe have seen quite the recovery this year, thanks to strong LNG imports. The gap to the 5-year average has narrowed significantly, which has left inventory levels at 52% full, not far off from the 5-year average of a little under 55%, and well above the 43% we saw at this stage last year. However, a prolonged outage will raise concerns over the ability of the EU to build enough storage going into the next heating season, and potentially see the EU falling short of its target of having storage 80% full by 1 November.

We are already seeing some worrying signs for storage. European storage levels fell for the first time on the 14 June sine mid-April. Clearly this should not be happening in the injection season but reflects the lower flows along Nord Stream. This will be unsettling for the market and is likely to keep prices supported. If the Nord Stream disruption proves to be prolonged, expect further upside to prices.

European gas storage (% full)

Source: GIE, ING Research

The statements, opinions and data contained in the content published in Global Gas Perspectives are solely those of the individual authors and contributors and not of the publisher and the editor(s) of Natural Gas World.