Shale getting stingy?

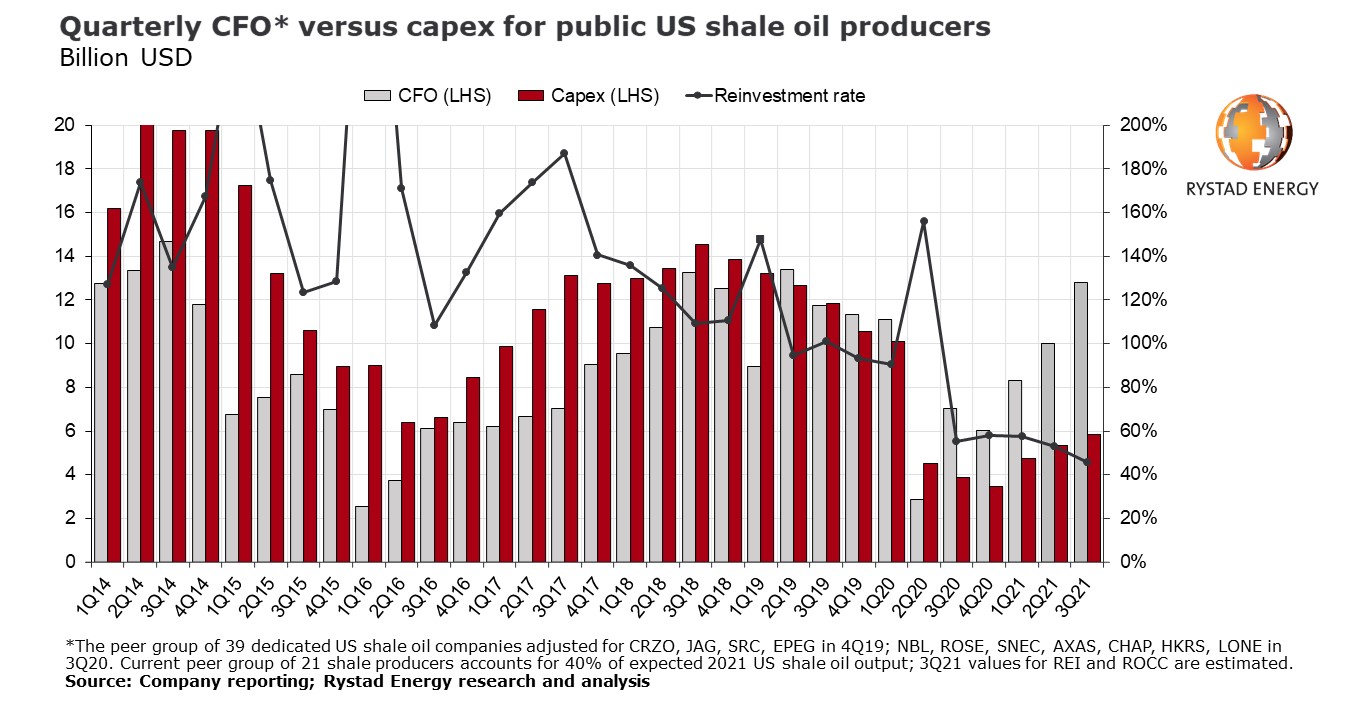

Reinvestment rates among US shale oil producers hit an all-time low in the third quarter of 2021, resulting in a record free cash flow for the quarter, and are projected to fall even lower by year-end according to a Rystad Energy analysis. The analysis focused on a peer group of 21 public US shale oil producers, excluding majors, that together account for 40% of the expected 2021 output.

The peer group’s combined reinvestment rate in the third quarter of 2021 was 46%, down from 53% over the same period in 2020 and way lower than the historical average of above 130%. The reinvestment rate is calculated by comparing shale producers’ oil and gas capex against their cash flow from operations (CFO). The CFO of the last quarter was the strongest since the second quarter of 2019.

|

Advertisement: The National Gas Company of Trinidad and Tobago Limited (NGC) NGC’s HSSE strategy is reflective and supportive of the organisational vision to become a leader in the global energy business. |

The analysis shows $7 billion in underspending by shale producers over the third quarter of 2021, comparing oil and gas capex with CFO. Operators managed to slightly increase peer-group quarterly capex in this year’s third quarter to $5.9 billion, up from $5.3 billion in the previous quarter, while further increasing CFO to $12.8 billion. All but one operator balanced spending in the third quarter of this year, reaching a new level of industry-wide cash balancing.

“Such a low reinvestment rate stands out for shale industry observers, especially as the peer group reported a record-breaking free cash flow (FCF) and earnings before interest, tax, depreciation and amortization (EBITDA) of $6 billion and $16 billion, respectively. But it’s not the end of the reinvestment slide,” says Alisa Lukash, vice president for North American shale at Rystad Energy.

Rystad Energy projections show that reinvestment will fall further to 40% in the fourth quarter of 2021. Also, for the first time since late 2018, the group’s combined net debt dropped below the eight-year average floor of $52 billion, coming in at $51 billion for the third quarter. Additionally, leverage ratios continued their consistent decline in keeping with the past three quarters.

Third-quarter results show several large independent operators ramped up spending in line with another financially robust quarter, in part due to the strong recovery in West Texas Intermediate (WTI) crude prices. Operators, as expected, started to communicate 7% to 15% cost inflation, with much of the impact anticipated to come in early 2022. However, this is expected to be absorbed by improved well productivity and capital efficiencies in most cases.

Combined third-quarter net income for the peer group amounted to $5.3 billion, double the income earned in the second quarter of 2021 and significantly higher than the sizable losses of $6 billion and $2.1 billion in the third and fourth quarters of 2020, respectively. EBITDA, meanwhile, recovered to $16.3 billion in this year’s third quarter, a level not seen historically. FCF across the peer group was $5.6 billion, a rise of $500 million from the previous quarter and more than double the $2.5 billion seen in last year’s final quarter.

Dividend payments jumped by 70% for the peer group in this year’s third quarter versus the second quarter. In comparison, the actual dividend-to-capex ratio increased to 26% compared to 17% in the preceding quarter. Further capital spending control by the industry was aimed at deleveraging and garnering stable shareholder support. Stock buybacks have predominantly been paused as the market recovered naturally with the WTI price increase. However, a few companies (CLR, FANG, PDCE) initiated buybacks amounting to $200 million.

For the first time since late 2018, the peer group dropped combined net debt below the eight-year average floor of $52 billion, reporting $51 billion for this year’s third quarter. Many operators mentioned revised hedging plans for 2022 due to lower expected leverage. Both leverage ratios – total debt to assets and total debt to equity – have consistently declined during the last three quarters. Despite more robust stock prices driving total equity up in 2021, the decline in leverage ratios has been partly offset by consistent debt issuance flared by merger and acquisition opportunities in the shale sector.

The statements, opinions and data contained in the content published in Global Gas Perspectives are solely those of the individual authors and contributors and not of the publisher and the editor(s) of Natural Gas World.