North Asian nuclear trends: implications for LNG [LNG Condensed]

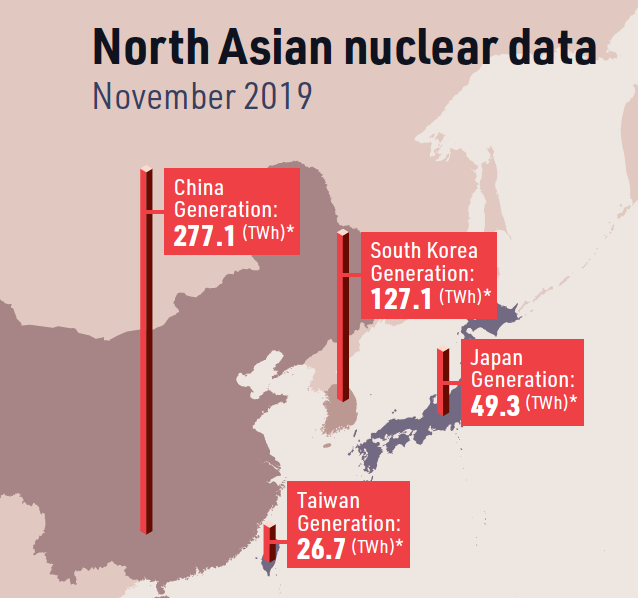

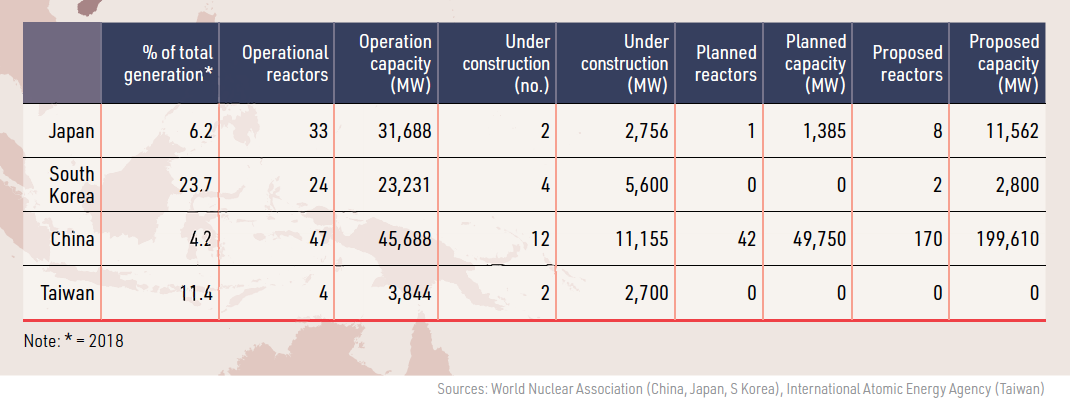

South Korea had 24 operating reactors with 23,231 MW of capacity at four sites in November 2019, according to the World Nuclear Association (WNA), with a further 5,600 MW under construction. The country produces a higher proportion of electricity from nuclear than anywhere else in North Asia, with its reactors generating 23.7% of output in 2018. The percentage increased to 28% from January to July 2019, according to the Korea Energy Statistical Information System (Kesis), as reactors closed in 2018 for maintenance and safety checks resumed operation.

The 25% year-on-year jump in nuclear output to 91.4 TWh in January-July 2019, combined with an increase in renewable output and fall in overall electricity supply, squeezed gas-fired output. Combined-cycle generation fell to 82.7 TWh from 93.2 TWh in the same seven-month period of 2018, according to the Korea Energy Economics Institute (KEEI).

|

Advertisement: The National Gas Company of Trinidad and Tobago Limited (NGC) NGC’s HSSE strategy is reflective and supportive of the organisational vision to become a leader in the global energy business. |

As a result, LNG use for power generation fell to 9.62 million mt (13bn m3) in January-July 2019 from 10.95 million mt in the same period of 2018. This in turn accounted for much of the decline in total LNG imports during the seven-month period, with arrivals falling by about 10% year on year to 22.93 million mt.

The downward trend has continued. Korea Gas Corporation data shows LNG sales to power generators fell to 11.75 million mt in the ten months to October 2019 from 13.56 million mt in the same period of 2018.

Policy direction

This is at odds with the May 2017 change in South Korean energy policy. President Moon Jae-in committed to the gradual phasing out of nuclear power and its replacement with renewable energy, with LNG seen as the key bridging fuel.

However, gradual is the operative word, with the phase-out yet to begin. In fact, the reverse is happening. In mid-2019, the 1,400 MW Shin Kori-4 reactor entered operation. A further four units with 5,600 MW of capacity are under construction for scheduled operation by 2024. The first of these, the 1,400MW Shin Hanul-1 reactor, could begin operating in 2020.

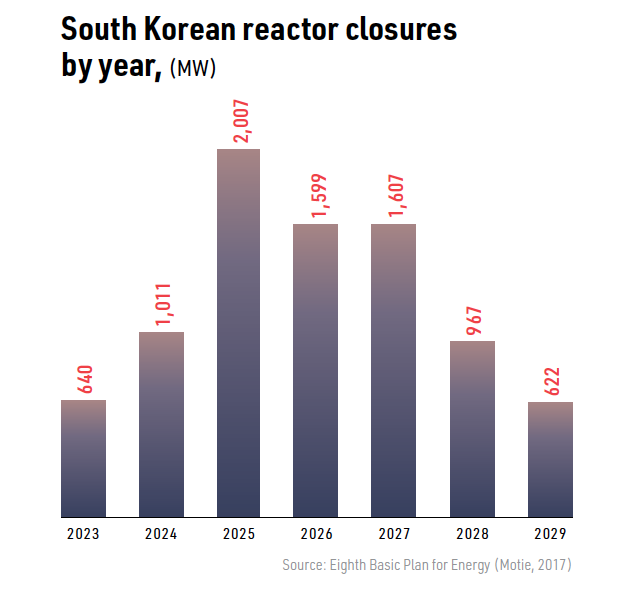

Partly offsetting this, ten reactors with 8,453 MW of capacity are due to close by 2030, according to the Eighth Long-term Electricity Plan issued in October 2017. But only two will close by 2025, meaning nuclear capacity will rise to 28.2GW in 2023 before declining to 20.4GW in 2030.

Mid-term outlook

The difficult near-term outlook this implies for gas is apparent from KEEI’s Mid-Term Energy Outlook, issued in October 2019.

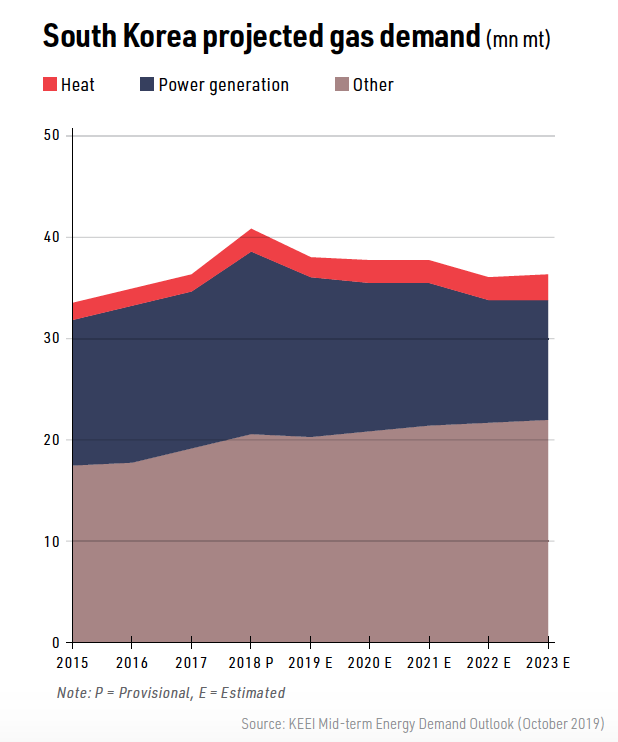

Nuclear output is projected to jump from 133.5 TWh in 2018 to 216 TWh in 2023, while gas-fired generation is projected to fall from 153.5 TWh to 100.8 TWh over the same period. Projected gas use in power generation falls in tandem, dropping from 18 million mt to 11.8 million mt, reducing overall gas demand from 40.9 million mt to 36.2 million mt.

How much LNG is actually used in South Korea will depend on factors other than nuclear output, not least how quickly the country’s stuttering economy recovers; whether renewable capacity can rise five-fold to 58.5 GW by 2030; and whether government support for coal-fired generation will succumb to fierce environmental opposition.

But the LNG surge in 2018 and slump in 2019 show that nuclear developments have a key impact on South Korean LNG use. At present, the projected impact is very much on the down side, but this could quickly change, if the reactor construction programme suffers extended delays or the nuclear industry is affected by incident or scandal as it has been in the past.

Japan LNG demand steady

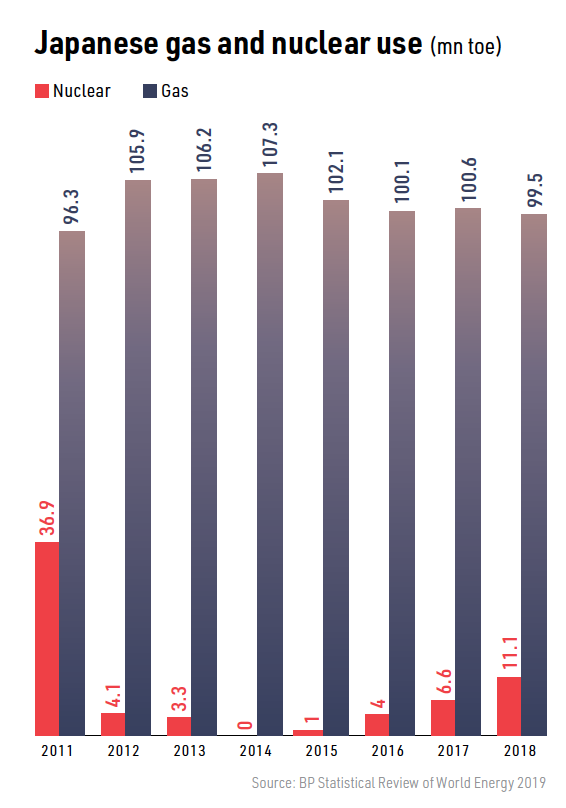

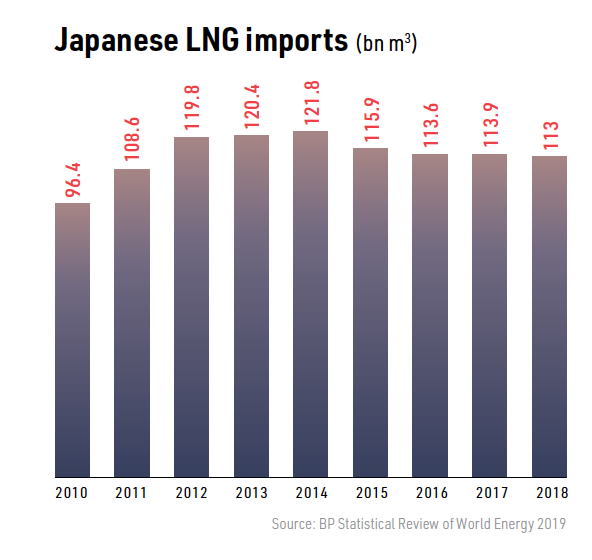

The inverse relationship between nuclear output and LNG use is less close in Japan than South Korea, but still significant. This was apparent in 2018 when four reactors resumed operation and the suspension of another – Ikata-3 -- was reversed. This contributed to a 1% on-year fall in LNG imports to 82.85 million mt, according to ministry of finance data.

By the start of 2019, nine reactors with 8,706 MW of capacity had resumed operation. They accounted for 49.3 TWh or 6.2% of total electricity in 2018, compared with 17.5 TWh and 2.2% in 2016.

A nuclear renaissance thus seemed under way. The Strategic Energy Plan approved in July 2018 envisaged that gas use in 2030 would be squeezed by a 20-22% minimum share for nuclear, as well as a 22-24% share for renewables and energy efficiency measures.

However, 2019 saw little activity, with no reactor restarts occurring. The restart of three units with 2,340 MW of capacity is proposed in 2020, but by no means certain.

Nor has 2019 seen much change in the status of 21 other reactors, 20,633 MW of which have regulatory approval to restart, but are under regulatory review, or have yet to apply to restart. One of the few changes occurred in November, when the 796 MW Onagawa-2 reactor secured regulatory approval for restart, but it must still overcome strong local opposition to renewed operation.

Restart stutters

The restart programme has been delayed not only by local opposition, but also by increasingly stringent regulatory and technical requirements. Notably, in April 2019, new conditions were attached to the implementation of anti-terrorism measures at reactors. This could lead to the temporary closure of some or all of the nine operating reactors in 2020.

This potentially would boost LNG use. In October, Kyushu Electric said its 846 MW Sendai-1 and Sendai-2 reactors could both be offline for eight to nine months in 2020-21, while work is done to meet the new anti-terrorism requirements.

Conversely, reactor restarts could eat into LNG’s share of the generation market in the course of the 2020s, but there are few indications that there will be a significant uptick in the pace of reactor restarts, or that all idled reactors will restart, meaning the government’s target of a 20-22% nuclear share by 2030 will be hard to achieve. Increased nuclear generation in any case tends to displace oil-fired generation before gas.

The slow progress in restarting Japanese reactors, combined with flat electricity demand and industry resistance to environmental organisations’ demands to slash coal burn, mean Japan’s LNG use for power generation is likely to remain fairly steady in coming years.

China’s nuclear build out

China is the region’s dominant nuclear generator, with output reaching 277.1 TWh in 2018. According to the WNA, it hosted 47 operational reactors with 45.7 GW of capacity in November 2019. China also accounts for a significant proportion of the regional and global stock of reactors under construction or planned.

Most operating Chinese capacity was commissioned relatively recently, with eight reactors with 10 GW joining the grid between June 2018 and June 2019 alone. Average reactor age is low at about seven years.

However, for all its success in implementing a large number of nuclear projects at a relatively fast pace, China will almost certainly miss its 2020 target of 58 GW. The 2030 targets of 120-150 GW and 8-10% of total electricity output also appear very ambitious.

This is because the pipeline of projects under construction has dwindled. The start of work on Zhangzhou-1 in October 2019 was China’s first construction start since December 2016. In November 2019, twelve reactors with 11,155MW of capacity were under construction, down from 20 in 2017.

However, this does not necessarily represent an opportunity for LNG.

Such is the scale of China’s generating sector that its reactors accounted for little more than 4% of total electricity output in 2018, even though their output increased by almost 20% year on year. The nuclear sector’s performance had no discernible impact on the country’s gas-fired generation plants, whose output grew by 10.3% to 223.6 TWh in 2018.

While gas-fired and nuclear plants do compete for investment funds and grid access at local level, their prospects are not intrinsically linked in the same way as other regional jurisdictions. Indeed, the key source of competition for both is renewable capacity, because of plummeting wind and solar capital and generating costs. China may be one of the key markets for LNG, but its requirements appear unlikely to be profoundly influenced by nuclear developments.

Taiwan

Taiwan hosts four operating reactors with 3,842 MW of capacity at Kuosheng and Maanshan, according to the International Atomic Energy Agency. Nuclear output of 26.7 TWh in 2018 accounted for 11.4% of total generation.

.png) Government policy is to close all reactors by 2025, although a November 2018 referendum sought to repeal legislation requiring a ‘nuclear-free homeland’ by 2025. This led pro-nuclear groups to demand existing reactors operate beyond 2025 and construction resume on the 2,700 MW nuclear plant at Lungmen, work on which was suspended in 2015.

Government policy is to close all reactors by 2025, although a November 2018 referendum sought to repeal legislation requiring a ‘nuclear-free homeland’ by 2025. This led pro-nuclear groups to demand existing reactors operate beyond 2025 and construction resume on the 2,700 MW nuclear plant at Lungmen, work on which was suspended in 2015..png)

Lungmen would be unlikely to start operating until the 2030s, given that state utility Taipower has said it would take six to seven years to resolve issues relating to reactivation of the project before construction could even start. However, if the opposition KMT took office some existing reactors might continue operating beyond 2025.

This would affect gas-fired generation, which the government projects will produce 50% of electricity -- or about 157 TWh -- in 2025. While licensing and waste disposal issues could constrain output, nuclear might thus reduce gas-fired generation by 15-30 TWh/year, trimming projected power generation gas use of 22.1mn mt in 2025 by some 2.2-4.4mn mt.

Available Exclusively to NGW Subscribers:

Volume 1, Issue 12 - January 6, 2020

|

LNG Condensed brings you independent analysis of the LNG world's rapidly evolving markets. Covering the length of the LNG value chain and the breadth of this global industry, it will inform, provoke and enrich your decision making. Published monthly, LNG Condensed provides original content on industry developments by the leading editorial team from Natural Gas World. LNG Condensed is your magazine for the fuel of the future. Sign up to NGW Basic FREE or to NGW Premium now to receive LNG Condensed monthly (you will find every issue of LNG Condensed in your subscriber dashboard)

|

In this Issue:Editorial: Climate Resilience There were many major achievements for the LNG industry over the course of 2019. Final investment decisions were taken on a swathe of next generation LNG projects in Russia, Mozambique, Qatar and the US. Even Nigeria LNG’s long overdue expansion got the go-ahead. There was clear evidence of the LNG market’s growing maturity in the form of the steep rise in liquidity in futures contracts linked to S&P Platts JKM price assessment, while BP’s publication of its LNG trading terms and conditions should aid much-needed contract standardisation. The growth of portfolio players, more diverse pricing mechanisms and the gradual disappearance of destination restrictions all bode well for increased international LNG trade. The LNG industry is booming, but is it ready for climate change? The LNG industry is set for continued, rapid expansion. As growing gas use now outweighs the emissions benefits of reduced coal consumption, and renewables are increasingly competitive, the environmental and economic case for LNG is eroding. Companies need to take a hard look at their business models and make radical changes – otherwise their image will quickly move from being part of the solution to being part of the climate change problem. Dili to go it alone in high stakes gamble The government of Timor-Leste has bought out foreign partners in the planned Greater Sunrise project to ensure the scheme’s LNG plant is built on domestic soil, but raising the fi nance for development is unlikely to be easy. Meanwhile, gas is running out on the Bayu Undan field, on which Dili is heavily dependent for state income. North Asian nuclear trends: implications for LNG North Asia accounts for a quarter of operational nuclear capacity worldwide, and about two-fifths of the capacity under construction or planned. But the prospects for nuclear power in the region vary widely, as do the implications for LNG requirements. Country Focus: Bangladesh’s LNG demand prospects Bangladesh is a newcomer to the world of LNG, but promises to become a substantial market with imports reaching 30mn mt/yr by 2041. Yet it would be foolhardy to say this demand is set in stone. Actual consumption depends on an ambitious industrialisation strategy and infrastructure delivery in all areas which could both benefit and detract from LNG demand. Project Focus: Rio Grande LNG US company Next Decade could hit the headlines early in 2020 if, as billed, it takes a final investment decision (FID) on its Rio Grande LNG project, the largest of four US LNG plants to receive final approval in November from the US Federal Energy Regulatory Commission (Ferc). Rio Grande LNG is located at the relatively uncongested Brownsville deepwater port on the US Gulf Coast. Technology Focus: FRSUs - The LNG industry’s flexible friend The growing popularity of floating storage and regasification units (FSRUs) is an integral part of the LNG market’s increasing flexibility. |

|---|