Lifting Sanctions on Iran: Implications for the Global Oil Market

After more than a decade of tough negotiations, the global oil industry expects to welcome Iran back into the market. On July 14, 2015, the P5+1 (the five permanent members of the United Nations Security Council—China, France, Russia, United Kingdom, United States—plus Germany), the European Union, and Iran agreed on a Joint Comprehensive Plan of Action (JCPOA). The JCPOA limits the Islamic Republic's nuclear program in return for relief from oil and financial sanctions.

If implemented, the landmark agreement will reopen the Iranian economy to global trade and recover billions of dollars in frozen assets. Most importantly, investment and technology-starved Iran will be able to rehabilitate its energy sector, which has been hit hard by international sanctions.

Although many obstacles remain before Western oil companies can do business there, the question of whether Iranian crude will reach the market is one of when rather than if. Based on the pace at which nuclear equipment is removed at uranium-enrichment facilities, sanctions against the Islamic Republic might be lifted as soon as early next year. The article seeks to analyze the implications of Iranian sanctions relief for the global oil market.

Nuclear-related Sanctions on Iran and their impact on the country’s energy industry

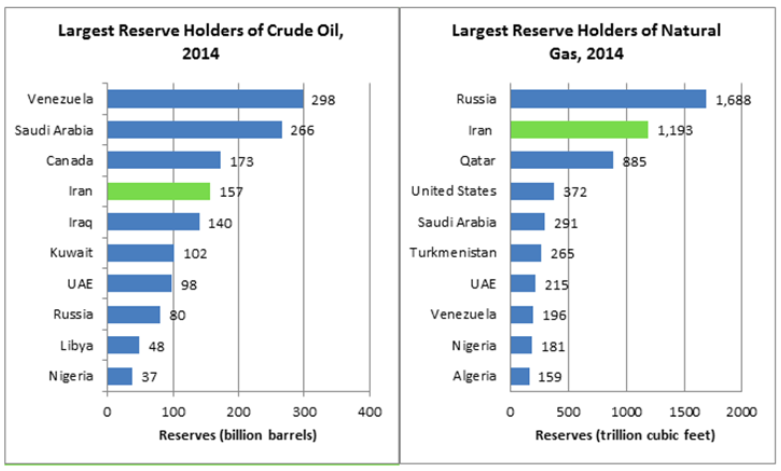

While Iran enjoys the world's fourth-largest proven crude oil reserves and the world's second-largest natural gas reserves, its production and export potential has remained largely unutilized as a result of the nuclear related sanctions. The sanctions have had a major impact on Iran's energy industry and have caused a number of cancellations or delays in its oil and gas upstream projects.

Source: U.S. Energy Information Administration

Nuclear-related sanctions on Iran date back to September 2005, when the International Atomic Energy Association (IAEA), the UN’s nuclear watchdog, found that the country was violating its treaty obligations in regard to the uranium-enrichment program. Since then, numerous sanctions have been imposed by various governments and international institutions, including the United States, United Nations and the European Union, mostly targeting Iran’s oil and financial sectors. The sanctions have sought to cut Tehran’s access to nuclear-related materials, and to exert economic pressure on the Iranian government to cease its uranium-enrichment program.

Rounds of sanctions enacted by the US and the EU in late 2011 and mid-2012 had an especially significant impact on Iran's energy sector. Besides boycotting Iranian crude, the sanctions dramatically limited Iran’s ability to export its oil by cutting the country off from London-based International Group of Protection and Indemnity (P&I) Clubs, which had provided Iranian oil carriers with insurance and reinsurance. As the European P&I clubs are responsible for the majority of insurance policies for ocean-going ships and cover around 95 percent of tankers worldwide, the insurance ban became a serious barrier to exporting Iranian crude.

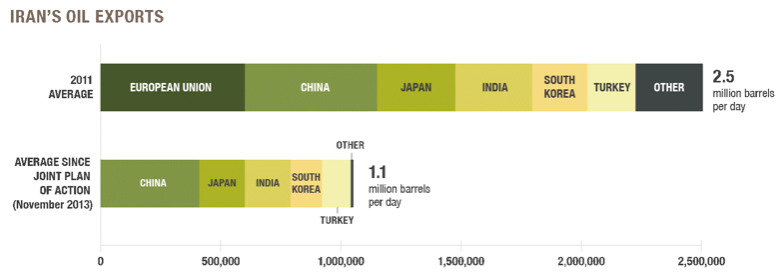

As a result, Iran’s oil exports dramatically declined from around 2.5 million barrels per day (mb/d) in 2012 to 1.1 mb/d today. In addition, only six buyers were allowed to import crude from Iran – China, Japan, India, South Korea, Turkey and Taiwan – down from 21 before the sanctions were implemented.

Source: Congressional Research Service/ CFR

Three-stage increase of Iranian crude export

According to the terms of the JCPOA, sanctions will be lifted once the IAEA submits a report to the UN Security Council confirming Iran's adherence to the nuclear restrictions of the agreement. The most recent statistics indicate that Iran has already disconnected almost a quarter of its uranium-enriching centrifuges in less than a month. Based on the pace at which nuclear equipment is being removed from uranium-enrichment facilities, sanctions against Iran might be lifted as soon as early next year. In addition, the Islamic Republic is holding parliamentary elections on February 26, and President Rouhani's team should gain electoral support if the sanctions have been lifted by then.

Amid the anticipated sanctions relief, Iran is already preparing to ramp up its crude output. The country’s oil exports will likely rise in three stages.

The first stage will be the immediate release of the crude currently stored on tankers that it has not been able to sell due to sanctions. Since data on Iranian crude oil storage is not publicly available, conflicting reports have circulated, with estimates ranging from around 10 million barrels up to 50 million of barrels. In fact, many experts analyze crude volumes by calculating oil tankers and measuring how deep the ships float in the water. According to the US Energy Information Administration, Iran stores around 30 million barrels, more than half of which is condensate, while the rest is mainly medium, sour crude oil.

The pace of the sales also remains highly uncertain and will depend on a number of factors, including the price of crude and the availability of customers. In theory, Iran could release all of its stockpiled crude and condensate volumes in just a month or two. However, a dumping policy would be damaging, as it would force Tehran to accept larger discounts, thereby, significantly reducing its revenues. Most probably, the volumes in storage will be released at the pace of 100,000-250,000 barrels per day in around six months.

Thus Iranian crude will hit global markets long before the Islamic Republic starts pumping more oil. Whatever volumes are coming, they will surely put downward pressure on an already oversupplied market.

The second stage will be the re-opening of the wells Iran has been forced to shut down, and the revitalization of mature oil fields currently experiencing production decline. Although Iranian officials claim to return to pre-sanctions levels within a couple of months, most probably it should take around a year to produce an extra 1 million barrels of crude oil. Many existing reservoirs have been abandoned for decades, and will need significant investments and technology to offset falling reservoir pressure and maximize production capacity.

The priority destination for Iran’s rising crude output, according to the Iranian oil minister Bijan Zanganeh, will be Asian markets, where oil demand is still growing. Due to sanctions, Iran’s Asian share was largely displaced by Saudi Arabia and Kuwait, whose crude contents are chemically similar. In addition, Tehran will find itself competing with Russia, which has significantly increased its market share in many Asian countries, thanks to a pipeline to the Pacific and China.

Tehran is also keen to reclaim its market share in Europe, where additional Iranian barrels will be competing with similar sour quality crude from Russia, Iraq and Saudi Arabia, causing producers to grow still more competitive on pricing. Prior to the sanctions, Iran supplied around 1 mb/d of high-sulphur sour crude to European markets – mostly to Mediterranean refineries in Italy, Greece and Spain. Today, however, the deliveries are limited to just 100,000 barrels per day for Turkey.

According to the World Bank's simulations with a multi-country, multi-sector computable general equilibrium (CGE) model, without any policy interventions by OPEC and other oil producers, the resumption of Iran’s crude exports to pre-2012 levels should decrease international oil prices by around 14 percent. Assuming that Brent crude is traded at today's $38 (December 14, 2015) per barrel, oil prices should drop to around 33 USD.

Iran's potential return to pre-sanctions levels of crude export could also upset the fragile balance that has been established within OPEC. It is still unclear how the organization is going to accommodate Iran's possible increase in crude production amid the current global supply glut. In December 2011, OPEC agreed to cancel individual country quotas and set a collective ceiling of 30 mb/d. In reality, however, the organization dramatically exceeds its collective quota and currently pumps around 31.76 mb/d, mostly from Saudi Arabia and Iraq, OPEC’s top two producers.

Moreover, with Indonesia rejoining OPEC as of January 1, 2016, and bringing additional 800,000 barrels per day, the bloc’s de facto production will increase to around 32.56 mb/d. In this regard, OPEC was expected to adjust the ceiling at its December meeting to accommodate Jakarta’s return to the organization, but no changes were introduced. Thereby, OPEC’s output target can be considered as more of a guideline than a strict limit. Guided by its largest producer Saudi Arabia, the bloc will most probably continue pumping crude at near-record levels in a bid to maintain market share and squeeze higher-cost shale producers in the US.

In the third stage, Iran will attempt to develop its new oil fields. The Islamic Republic plans eventually to increase oil production to more than 5 million barrels a day by 2020. For that, according to the head of the National Iranian Oil Company and deputy oil minister Rokneddin Javadi, the country will need around $100 billion over the five years. Raising such a huge investment amid the current low oil prices would be a challenging task for Tehran.

Nevertheless, investments in Iran's upstream oil projects should be well worth the reward for international energy majors, which are already in preliminary discussions with Tehran. The country holds the world's fourth-largest proven crude oil reserves, with most of them located onshore, making development costs well below world averages. Market Realist, an investment research and analytics firm, estimates Iran's cost of crude production at $15 per barrel, which is way below shale, deep water and oil sands operations. According to the National Iranian Oil Company, production costs are even lower, averaging at $5-10 a barrel. In addition to favorable geology conditions making crude production cheap, Iran’s stable political regime (in comparison to neighboring countries) and its unique geographical position, with access to the Caspian Sea and the Persian Gulf, will prove attractive to international energy companies.

Iran’s new petroleum contract model

In an attempt to lure foreign investors to its energy industry, Iran has also introduced a new contract model, putting an end to a two-decade old buyback system that has prevented international oil companies from booking reserves or taking equity stakes in Iranian companies. Although Tehran has updated the buyback model twice since it was first released, the short-term risk service contracts have been unpopular among foreign energy companies due to their inflexibility and limited returns.

The new model, called Iran Petroleum Contract (IPC), aims to make the energy sector financially attractive to international oil companies by offering more flexibility on price fluctuations and investment risks. Under some circumstances, the IPC also allows reserves to be booked, though international oil companies would still not own fields. In addition, the new model extends project involvement period to 15-20 years, and in some cases up to 25 years, allowing for much longer cost recovery after first production.

Under the new contracts, foreign investors will also be required to partner with Iranian oil companies in running the projects. Potential investors are leading European energy majors, including Total, BP, Shell, Eni and OMV. All of them have recently met with Iranian oil executives, and are keen to exploit the country's abundant oil reserves once sanctions are lifted.

While European energy executives along with the Russians and Chinese line up do to business in a post-sanctions Iran, their American counterparts remain sidelined due to an existing ban prohibiting US firms from dealing with Iranian officials.

Conclusion

Based on the pace at which nuclear equipment is removed from uranium-enrichment facilities, sanctions against Iran could be lifted as soon as early next year. When sanctions are eased, Tehran will ramp up its crude exports in three stages.

First, the world oil market will see the immediate release of Iran's stockpiled crude and condensate, totaling around 30 million barrels. The release will be gradual, as dumping the market would not be in Tehran's interests. Thus, Iranian crude will hit the market long before the actual increase in production. Whatever volumes are coming, they will put downward pressure on global crude prices.

In the second stage, Iran will restore the wells it was forced to shut down and abandon due to the sanctions regime. It will allow the country to add an extra million barrels per day, to return to pre-sanctions export levels of 2.2 million. In an attempt to reclaim its market share, Tehran will be targeting, first of all, Asian and European markets, where the Iranian barrels will be competing with similar sour quality crude from Saudi Arabia, Iraq, Kuwait and Russia. Finally, Iran's full return to the crude market could also create a conflict of interests within OPEC over the market share issue and collective output target. Given that OPEC is unlikely to alter its collective ceiling quota, extra output from Iran will send crude prices down.

Finally, the third stage will be the development of new fields to take crude production level to more than 5 mb/d by 2020. Despite low oil prices, international oil companies are keen to invest in Iran. The country’s favorable geological conditions making crude production cheap, while its relatively stable political regime and direct access to waterways will prove attractive to international energy majors. In addition, Iran has recently updated its petroleum contract model making investments in the country's energy sector more rewarding.

Akhmed Gumbatov

Project Manager at the Caspian Center for Energy and Environment of ADA University