[GGP] Fully decarbonising Europe’s energy system by 2050

Decarbonising Europe’s energy system – the scale of the challenge

In a study recently published by Pöyry it highlights the scale of the challenge to fully decarbonise Europe’s transport, heat and power systems by 2050 as part of meeting the ambition within the Paris climate change agreement for limiting the global temperature increase to 1.5ºC..png)

This stretching ambition is a significant challenge for all stakeholders, from policy makers and public acceptance to developers of new technologies and those charged with delivering the infrastructure necessary to facilitate the energy transformation. Meeting the Paris ambition is particularly challenging for some sectors, e.g. industry, where its CO2 emissions in 2014 are already over three times the economy wide limit for 2050, a 95% reduction compared to 1990 levels. Such an ambitious reduction requires a full decarbonisation of the energy sector (transport, heat and power) alongside a significant reduction in other sectors (shipping, aviation, agriculture, food, other land use and waste), a process likely to cost many billions of Euros over the next 30 years.

The study evaluated two potential pathways to a decarbonised Europe; a ‘Zero Carbon Gas’ pathway, where biomethane, hydrogen and CCS are part of the technology options allowed to economically compete in the solution; and an ‘All-Electric’ future, where only electrification of all transport and heat is permitted. Although other pathways may be possible, it is the comparison of these two which is instructive for understanding the risks and challenges.

‘Zero Carbon Gas’ pathway

The ‘Zero Carbon Gas’ pathway represents a future where economics determine which technologies are deployed to fully decarbonise the energy sector. The gas industry is allowed to adapt to the requirements of a decarbonised system and provides zero carbon energy in all sectors.

In the non-process heating sector a combination of natural gas district heating (with CCS), hybrid heat pumps and stand-alone hydrogen boilers are required to meet the decarbonisation targets. This transition is reliant on a number of new technologies such as hybrid heat pumps and new fuels (e.g. hydrogen and biomethane) becoming commercially available.

As hybrid heat pumps utilise electricity in warmer conditions and biomethane and hydrogen during periods of colder temperatures, hydrogen appears in small quantities by 2030 and then expands as the supply chain develops.

Decarbonisation in the transport sector is achieved through a mixture of hydrogen vehicles, mostly in the freight sector, and electric vehicles, primarily in the passenger sector. Nearly 100m hydrogen-powered vehicles are deployed alongside 330m electric vehicles.

The expansion of electricity use in transport and heat means that total European electricity demand will increase by 60% in 2050. Solar and onshore wind are the main drivers of the required 150% capacity increase across Europe. Interconnector capacity grows strongly, but nuclear capacity falls over time as there are cheaper options available. The resulting generation mix is therefore dominated by renewables as the cheapest form of zero carbon generation.

'All-Electric’ pathway

This pathway builds upon the assumption that only electrification can achieve decarbonisation and policies are put in place to prevent the development of ‘Zero Carbon Gas’ alternatives, resulting in new nuclear and biomass build.

Heat pumps become the dominant technology in non-process heating, with air-source heat pumps in urban environments and ground-source heat pumps in rural areas. In many Northern European countries, air-source heat pumps are deployed alongside an electric resistive back-up system to cover time periods when the ambient outside temperature falls below working limits for stand-alone heat pumps (assumed to be -15°C). The options in process heat are more limited, as electric heating can only play a limited role. The remaining demand – currently met with coal, oil and gas – switches to biomass as the only practical zero carbon alternative that can support high temperature load needs. This leads to large biomass requirements in this pathway which are assumed to be sustainable. Heat from combined heat and power, which converts from fossil fuels to biomass, is also used.

Decarbonisation is achieved in the transport sector by fully electrifying all road vehicles and all trains as other options are not allowed in this pathway. This includes heavy goods vehicles, which assumes that there is successful development of very large battery systems and supercharging facilities to ensure range requirements are met. This pathway estimates that 432m electric vehicles will be on the road in 2050 across Europe.

The electrification of transport and heat means total European electricity demand increases by approximately 180% from 2020 to 2050, whilst total renewable generation in 2050 is around 80%. More than five times the amount of nuclear generation required in the 'Zero Carbon Gas' pathway is needed to help balance intermittency alongside smart demand side response. Since many countries do not allow nuclear power, those countries that do, especially France, the UK, Poland and Czech Republic, are expected to build the bulk of the new 190GW. European-wide electricity interconnection approximately doubles to more than 300GW by 2050 to enable sharing of all generation sources.

Risks, opportunities and costs

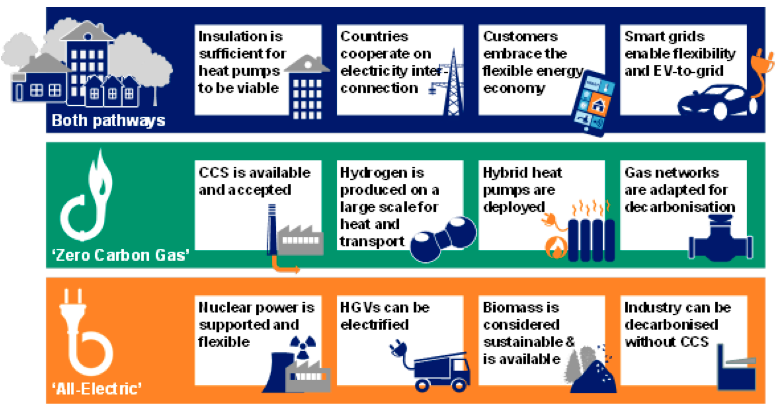

In order for the envisaged pathways to be feasible, several prerequisites need to be met:

ANY DECARBONISATION PATHWAY CAN ONLY BE ACHIEVED IF…

• Insulation is sufficient for heat pumps to be viable: Since heat pumps provide a lower amount of heat compared to boilers, it is important that buildings are sufficiently insulated for heat pumps to be viable. In order to deploy heat pumps on the envisaged scale, significant expansion is required in the supply chain.

• Countries co-operate on electricity interconnection: In order to avoid overbuilding generation capacity and maximise the value of intermittent renewables, a substantial increase in interconnection between countries is required.

• Customers embrace the flexible energy economy: Frameworks need to be put in place to allow smart and flexible services. Consumers need the right incentives so that they embrace flexibility and contribute actively (or automatically) to the energy economy, including smart appliances, heating and EV charging.

• Smart grids enable flexibility and ‘EV-to-grid’: In addition to the frameworks, the technical fundamentals need to be in place to allow smart operation of grids and appliances. This includes improved batteries that deteriorate less quickly when operated as required (two-way charging).

A ‘ZERO CARBON GAS’ PATHWAY CAN BE ACHIEVED IF...

• CCS is available and accepted: CCS allows gas to be used in a wide range of sectors (power generation, heat production, hydrogen production and industrial process output). Pipeline infrastructure needs to be built and adapted to transport the CO2 to the storage sites.

• Hydrogen is produced on a large scale for heat and transport: In order for hydrogen to be competitive, large quantities of methane reformers need to be deployed.

• Hybrid heat pumps are deployed: Reflecting poorer performance of air-source heat pumps in colder weather hybrid heat pumps are deployed in homes alongside boilers using biomethane or hydrogen. Such systems need to be available and ready for largescale deployment.

• Gas networks are adapted for decarbonisation: In most countries, the use of gases in heating remains high across the modelled period. These networks need to be adapted for decarbonisation (e.g. different usage patterns, conversion to hydrogen).

AN ‘ALL-ELECTRIC’ PATHWAY CAN BE ACHIEVED IF…

• Nuclear power is supported and flexible: A zero-carbon system based on electrification requires a significant contribution from nuclear power. This will be challenging from several perspectives: politically – acceptance is problematical across Europe; from a supply chain perspective – amount of new build required is as high as its historical peak; and technically – plants will be operated much more flexibly than today.

• HGVs can be electrified: The pathway focus leads to an electric heavy transport sector, with supported infrastructure.

• Biomass is considered sustainable and is available: The absence of CCS or any other alternatives leaves sustainable biomass as the only option to decarbonise heat for industrial processes that cannot be provided by electric solutions.

• Industry can be decarbonised without CCS: While this study only considers decarbonisation of the energy sector, not allowing CCS has wide-ranging consequences for the industrial sector. Without CCS, other more expensive solutions in industrial processes need to be found to avoid emissions – or operations need to scale down or relocate away from Europe.

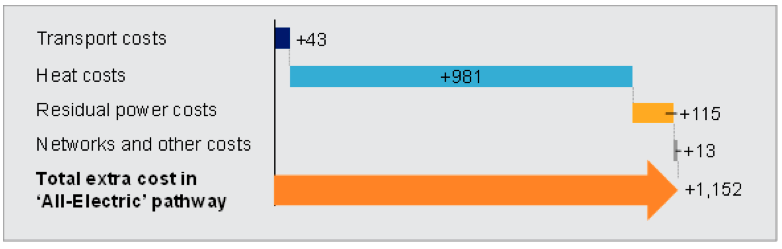

Total System Costs

Combining the analysis from all sector models with calculations of networks, supply and other costs produces the total system costs for each pathway. There are significant extra costs of €1.15tn associated with the ‘All-Electric’ pathway, which precludes CCS, biomethane and hydrogen. The largest differences occur in the heating sector, where both electricity and biomass fuel prices contribute to very high costs, and in residual power costs, which are mainly associated with the extra costs of power generation, especially nuclear, in the ‘All-Electric’ pathway.

The final outcome of a fully decarbonised ‘All-Electric’ solution is €94bn more costly per annum in 2050 than the ‘Zero Carbon Gas’ alternative. This is especially the case for the transport and heat sector costs which amount to €113bn of additional costs p.a. in 2050.

Key messages and recommendations

The key messages and risk mitigation factors that all stakeholders should consider based on the analysis in this study are the following:

- Keeping options open is critical to managing risks, costs and security of supply. A pathway that precludes options, e.g. CCS, could lead to higher investment costs than necessary (e.g. in power generation or networks) and increased risks. Accordingly, it is prudent to keep as much flexibility in the technology options available.

- Utilising Zero Carbon Gas options as part of the energy mix, especially in transforming heat, comes at a saving of over €1,150bn compared to an ‘All-Electric’ world only.

- The future for small vehicles is electric, but for larger vehicles hydrogen is a better option.

- CCS deployment allows industry to decarbonise not only energy but also process emissions.

- Power generation will be dominated by renewable technologies - especially solar PV and onshore wind - with some support from flexible zero carbon technologies, which comes from nuclear in an ‘All-Electric’ world of from Hydrogen and CCS in a ‘Zero Carbon Gas’ world. It makes economic sense to deploy these where the natural resource is most prevalent.

Interestingly the findings also predict a major shift in the future, where demand balances intermittent supply by utilising flexible EVs and electric heat. This mass deployment of smart-grid connected and flexible EVs will largely displace other flexibility providers like batteries and power-to-gas, by removing many periods of excess renewable generation.

The good news for all stakeholders is that this study has shown that it is feasible to fully decarbonise Europe’s transport, heat and electricity sectors by 2050. However, achieving this will require significant investments and requires a major transformation across all three sectors regardless of which particular pathways stakeholders chose to follow.

The statements, opinions and data contained in the content published in Global Gas Perspectives are solely those of the individual authors and contributors and not of the publisher and the editor(s) of Natural Gas World.