Eastern, Central Europe bolster domestic gas supply to offset Russian losses [Gas in Transition]

Oil and gas producers across eastern Europe are stepping up efforts to find and produce domestic gas as availability of Russian supply dwindles and imports from alternative, more expensive sources are forced to rise. The efforts include both heightened exploration and accelerated development plans for fields that have already been found. These include Romania’s Neptun Deep project, which was given the go-ahead by partners OMV Petrom and Romgaz in June this year. The project is located off the coast of Romania in the Black Sea, and is expected to incur development capex of about $4.4bn, mostly during 2024-26. Production is expected to total over 100bn m3 (or 700mn barrels of oil equivalent), at a rate of 8bn m3/yr, with first gas scheduled for 2027.

The new production (along with existing output) should cover the majority of Romania’s gas consumption of around 12bn m3/yr and leave some surplus for export, providing considerable relief for regional consumers. In a June report, the OIES said the implications were significant for both Romania and the region, “extending into pricing and hub formation, decarbonisation through lignite substitution, replacing Russian supplies and infrastructure creation.” It said that, at a price of €38/MWh (currently prevailing in the market), the value of the recoverable natural gas would be worth €44bn. Unit production cost is estimated at an average of $3/boe (or $1.76/MWh) for the life of the field.

OMV Petrom, which is majority-controlled by Austria's OMV, repeatedly deferred its investment decision in Neptun Deep over several years. The Romanian authorities improved terms in 2022 in the form of an amendment to the country’s Offshore Law, encouraging the group to move forward. And then, following Russia’s invasion, the project quickly moved up the priority list. During this period, ownership structures changed, with OMV Petrom becoming the project’s operator, after ExxonMobil sold its 50% stake to Romanian state-controlled gas company Romgaz.

Elsewhere in Romania, heightened onshore exploration has resulted in finds of around 30mn boe of gas near existing fields and infrastructure in the south of the country. The discoveries, made by OMV Petrom, are the largest for many years and occurred in three areas, with the biggest in the Verguleasa area. The domestic activity is being encouraged not just by more commercial opportunities in the wake of reduced Russian supply, but also by a government keen to enhance energy security, and more finds are expected.

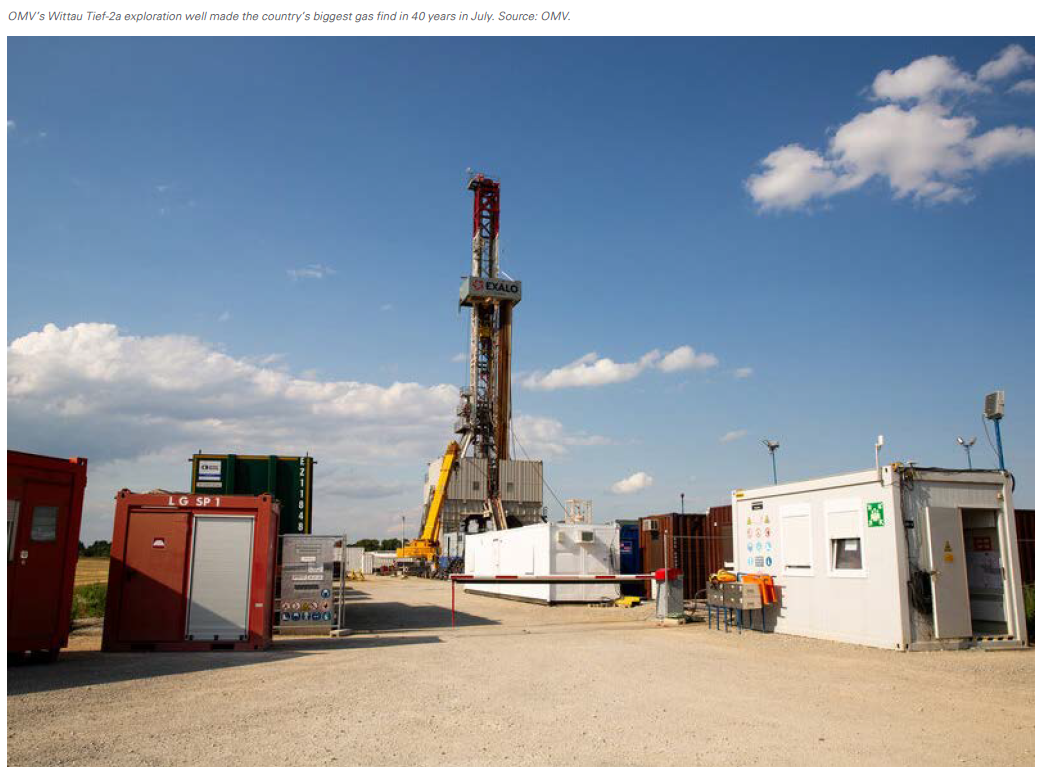

Austria finds gas

Meanwhile, earlier in the year in Austria, OMV said the Wittau Tief-2a exploration well had found the country’s largest natural gas field in 40 years. The OMV-operated well is in Lower Austria and was drilled to a final depth of 5,000 m over five months. A preliminary evaluation indicates potential recoverable resources of about 28mn boe or 48 TWh, and once developed the find is expected to double the country’s gas output.

OMV is currently considering different options to further appraise the field, as well as a fast-track development in conjunction with the OMV-operated natural gas facility in Aderklaa, situated 10 km from the new discovery. There have also been smaller gas discoveries in neighbouring Poland, which ended its reliance on Russian gas during 2022, as well as calls to renew drilling for what are believed to be extensive shale gas resources (that had once attracted Exxon Mobil and Chevron).

OMV is currently considering different options to further appraise the field, as well as a fast-track development in conjunction with the OMV-operated natural gas facility in Aderklaa, situated 10 km from the new discovery. There have also been smaller gas discoveries in neighbouring Poland, which ended its reliance on Russian gas during 2022, as well as calls to renew drilling for what are believed to be extensive shale gas resources (that had once attracted Exxon Mobil and Chevron).

The Austrian find will be particularly welcome. While neighbouring Germany and the Czech Republic have both reduced Russian gas imports to zero, Austria, like Hungary, has made little headway in reducing its reliance on Russian gas. However, change may soon be forced, because Ukraine has warned Austria that it will not renew its transit contract with Russia’s Gazprom next year – as reported by Ukranews on August 4. Austria is the main recipient of Russian gas transported via the Ukrainian route, with small portions also going to Hungary and Italy.

Ukraine’s national gas company, Naftogaz, alongside the Gas Transport System Operator of Ukraine (GTSOU), signed a deal with Gazprom in December 2019 for five years. The agreement allowed for the transit of Russian gas to Europe via Ukraine, comprising 65bn m3 of gas in 2020 and 40bn m3 between 2021-2024, totalling nearly 5% of Europe’s total gas imports. Ironically, Ukraine had in the past always tried to increase the volumes, complaining that alternative Nord Stream routes starved the country of a valuable source of transit income.

Denmark squeezes more from Tyra

Also seeking to boost domestic output, Denmark is expecting to see its biggest field back in action shortly, with two gas turbines powered up at the Tyra gas field ahead of the project’s restart following a lengthy redevelopment project, according to operator Total Energies in early July.

Tyra was closed down in September 2019 so that the topsides of the field’s platforms could be replaced – although at one point there had been questions over whether it would restart at all. There were repeated delays, in part because of supply chain issues and other disruptions relating to the COVID-19 pandemic, as well as calls from environmental groups in government to shut it down permanently in pursuit of ambitious decarbonisation goals. But Russia’s invasion of Ukraine made the project more urgent and important to Denmark’s energy supply security – Denmark had its Russian gas supply completely cut off at the end of May 2022 after it refused to settle payments in rubles.

Once back online in Q4 2023 or Q1 2024, Tyra will supply Denmark and Europe with 2.8bn m3/yr via export pipelines to Nybro and Den Helder. The three new turbines each have a generation capacity of 35 MW. TotalEnergies operates Tyra with a 43.2% interest, while BlueNord has a 36.8% stake and Nordosfonden has 20%.

Azeri Solidarity Ring

As well as more domestic production and LNG deliveries, eastern Europe is also seeking more pipeline flows from Norway, Azerbaijan and even North Africa (via Italy). Austria, in particular, plans to increase supply from Norway, which is now the continent’s biggest supplier, and all will draw from LNG delivered at new and existing terminals on the Baltic and Adriatic Seas this winter.

In April, Azerbaijan signed a deal with four countries in the region, dubbed the “Solidarity Ring initiative.” The MoU was signed by Azerbaijan’s state oil and gas company SOCAR, and the national gas transportation operators of Bulgaria, Romania, Hungary and Slovakia (Bulgartransgaz, Transgaz, FGSZ and Eustream). It outlines plans for SOCAR to work with the other four companies as they upgrade their pipeline networks to facilitate deliveries of Azeri gas. Hungary has already said it will import Azeri gas within the framework of its participation in the deal.