A turning point for African gas? [Gas in Transition]

Growth in African natural gas production is set to accelerate to 10% annually over the 2022-26 period, the International Energy Agency (IEA) reported in its medium-term gas outlook report, up from an average of 2.5%/year in 2011-21, on the back of a raft of new LNG projects. However, the Paris-based organisation is less bullish in its demand forecast, projecting annual growth of only 3%, hindered by high prices and the fact that expected output growth is mostly export-orientated, in countries with under-developed gas markets, while demand growth in well-established markets is slowing.

Africa is home to close to one-fifth of the global population, and that population is also the younger and fastest-growing in the world. But it also has the lowest level of energy access – 43% have no access to electricity. It hosts more than 9% of global gas reserves while contributing 6% of global supply in 2022. It accounts for only 4% of global demand.

“Its significant natural gas reserves could turn Africa into a key player in the global gas market, while improving energy access for its rapidly growing population,” the IEA states.

On supply

Africa accounted for nearly four-fifths of new natural gas discoveries in the world in the past decade, primarily in Mozambique, Mauritania, Senegal and Tanzania. But development has been stymied by socio-political instability and security issues, making for a high-risk investment climate.

As a result, the IEA notes that there is a gap between the “potential” and the “actual” when it comes to gas production. The recent delays at LNG projects in north Mozambique due to insurgency risks are testament to this.

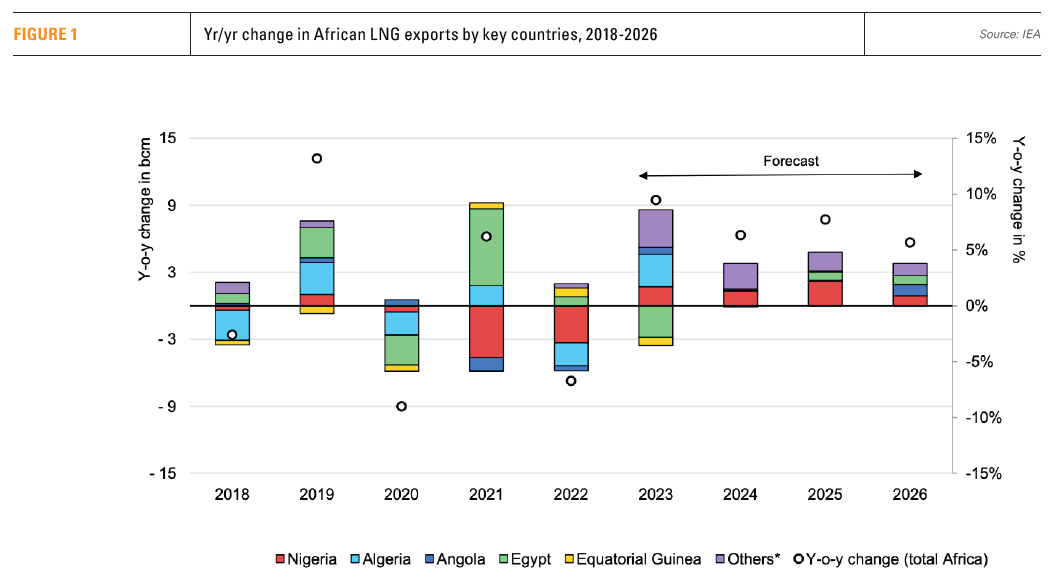

Nevertheless, momentum is building. Having reached 246bn m3 in 2022, the continent’s gas output is on track for 10% annual growth up until 2026, according to the IEA, as a result of gradually rising production in Algeria and Nigeria, and fresh supply in Senegal, Mauritania, Congo and Gabon.

Out of the gas that Africa produced in 2022, 36% was exported, of which 61% was delivered overseas in the form of LNG. The majority of the gas exported went to Europe, 60%. In the coming years, the share of African gas exported and exports in LNG form is set to rise, thanks to several key new LNG developments.

Out of the gas that Africa produced in 2022, 36% was exported, of which 61% was delivered overseas in the form of LNG. The majority of the gas exported went to Europe, 60%. In the coming years, the share of African gas exported and exports in LNG form is set to rise, thanks to several key new LNG developments.

Current African LNG export capacity is just below 100bn m3/year. But over the past decade, more than a dozen new LNG export projects were announced. And in the late 2010s, final investment decisions (FIDs) were taken on Eni’s Coral South FLNG in Mozambique and BP’s Greater Tortue Ahmeyim (GTA) LNG project straddling the maritime border between Mauritania and Senegal, followed by large projects like TotalEnergies’ Mozambique LNG and NNPC’s Nigeria Train 7.

Additional developments in the proposed pipeline include GTA Phase 2, ExxonMobil’s Rovuma LNG in Mozambique, Cameroon Phase 2 and Nigeria FLNG, yet to be greenlit. Overall, the new projects in sub-Saharan Africa could contribute 90bn m3 of annual LNG capacity by the end of the decade, though only 16bn m3 is set to be commissioned by 2026.

However, the IEA warns that “Africa’s track record on LNG export projects is not encouraging.”

“The Mozambique LNG project has been halted since 2021 following the declaration of force majeure due to security risks,” it says. “The GTA LNG project is encountering problems with cost overruns, environmental concerns and cost inflation. These problems are weighing on the prospects for investment decisions for other African LNG projects.”

The Russia-Ukraine conflict and the resulting European rush for LNG has spurred new export projects in Africa. Eni has finalised with Congo on its Marine XII FLNG project, while BP is looking to take an FID on the first phase of its Yakaar-Teranga LNG project off Senegal before the end of the year. Meanwhile, Shell and Norway’s Equinor announced in mid-May that they had finished up negotiations on the Tanzania LNG project, and expect to sign a host government agreement and a production-sharing contract in the near future.

All this said, the IEA cautions that “considering the long lead times of LNG projects, these commitments are not going to change the game for African LNG in the immediate future.”

“For the time being, the continent’s LNG activities will continue to be dominated by established players: Egypt, Algeria and Nigeria (and, to a lesser extent, Equatorial Guinea and Angola).”

Algeria and Egypt are likely to maintain current annual LNG capacity at about 40bn m3 and 17bn m3 respectively, it says.

The IEA also warns that African LNG could be crowded out of the market before it can bring its projects to bear.

“The window of opportunity to monetise the region’s significant gas resources could be limited, with US and Qatari projects expected to start delivering significant volumes by 2027, and the potential for LNG demand to fall from 2030 onwards, driven by decarbonisation targets,” the agency says.

On demand

African gas demand has nearly tripled since 2000, and no surprise that the biggest consumers are also the major producers and key transit countries in North Africa.

Total African gas demand came to 172bn m3 in 2022, but from sometimes double-digit growth in the last two decades, the IEA sees the annual increase slowing to 3% in 2022-26.

“New natural gas markets are emerging, mainly for power generation, as in Ghana, South Africa and Senegal, to meet growing electricity needs and replace liquid fuels,” the IEA says. “These new markets are supported by the development of production as well as the commissioning of new import infrastructure. The current environment of high prices and tight supply is particularly challenging for these price-sensitive emerging African markets and is likely to have a negative impact on the growth outlook for natural gas consumption.”

The issue is also that while growth in production in mature markets in North Africa is slowing, therefore restricting any demand increases in those countries, much of the continent’s projected output growth in the coming years will be seen further south in Africa. And in the latter region, new production projects are primarily geared towards exports, while the promotion of domestic gas use has fallen by the wayside.